At midnight, the help vanished. By morning, millions of Americans shopping for their own health coverage were staring at new monthly numbers that look less like insurance and more like a second mortgage.

Washington has been warning this cliff was coming for years. Then it arrived anyway. Now both parties are scrambling to explain why an affordability policy that touched more than 20 million people could not survive a deadline everyone knew.

At midnight, ACA subsidies will expire and health care costs for Americans across the country will skyrocket by thousands of dollars. This is a disaster for families who need access to affordable, quality care.

And it’s all because of Donald Trump and Congressional Republicans. pic.twitter.com/USrIglDPu4

— G (@stockguy61) December 31, 2025

The deadline hit, and the math changed overnight

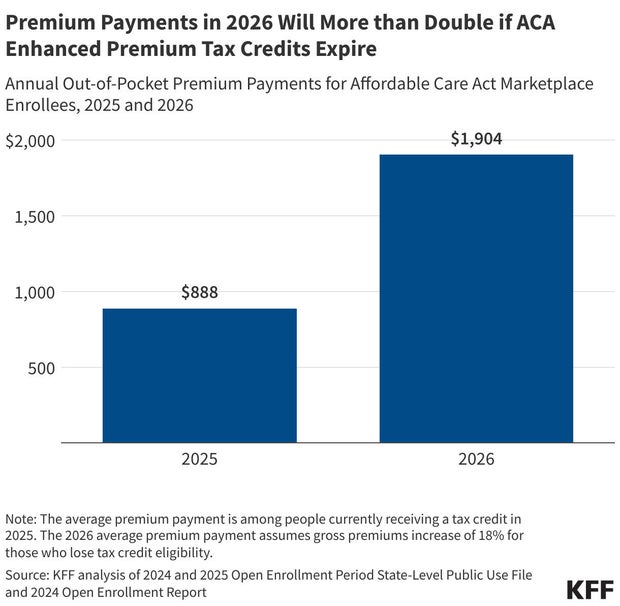

The enhanced premium tax credits that lowered costs for most Affordable Care Act marketplace enrollees expired as 2026 began, according to CBS News. Those subsidies were expanded during the COVID-19 era in 2021, then extended again so they would run through the start of 2026.

For many households, the enhanced credits did two politically potent things at once. They pushed some lower-income enrollees to $0 premium plans and capped premiums for higher earners at 8.5% of income. They also expanded eligibility to more middle-class earners.

With the expansion gone, enrollees who buy coverage on their own, meaning they do not get insurance through an employer and do not qualify for Medicaid or Medicare, are now absorbing the full price spike.

A government shutdown came and went, and the subsidies still died

The subsidy fight was not a quiet policy dispute. CBS News reported Democrats forced a 43-day government shutdown over the issue. Moderate Republicans publicly pushed for a solution, with an eye on 2026 politics. President Trump floated a path out, then backed off after conservative backlash, according to the same report.

In the end, none of it produced legislation in time. The credits expired anyway.

There may still be a second act. A House vote expected in January could offer another chance at reviving the subsidies, but the path is uncertain after the Senate already rejected competing bills in December.

What the receipts say: premium increases averaging 114%

The starkest number comes from health policy researchers tracking what happens when the enhanced credits disappear. KFF, a health care research nonprofit, estimated that the more than 20 million subsidized ACA enrollees are seeing premium costs rise by an average of 114% in 2026.

That average hides the personal horror stories and the policy risk. Some people see manageable jumps. Others see coverage priced out of reality.

Stan Clawson, a Salt Lake City freelance filmmaker and adjunct professor, told CBS News his monthly premium is moving from just under $350 to nearly $500. He said he lives with paralysis from a spinal cord injury and is willing to take on the strain because he needs coverage.

Katelin Provost, a 37-year-old single mother, told CBS News her premium is climbing from $85 a month to nearly $750. Her verdict lands like a vote of no confidence in the people arguing on cable news while families refresh enrollment pages: “I’m incredibly disappointed that there hasn’t been more action.”

The quiet danger for the ACA: younger people walking away

Analysts have long warned that when premiums jump, the healthiest customers often leave first. That is not just a household story. It is a math story that can push prices higher for everyone left in the pool.

An Urban Institute and Commonwealth Fund analysis projected that the higher premiums from expiring subsidies could prompt about 4.8 million Americans to drop coverage in 2026.

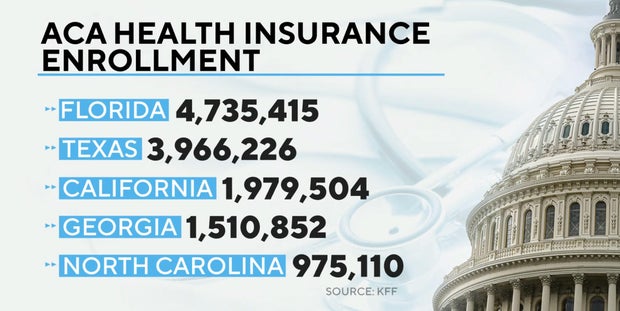

That kind of drop-off is not evenly distributed. KFF data shows Florida has the largest number of ACA enrollees, more than 4.7 million. Texas follows with more than 3.9 million, then California, Georgia, and North Carolina.

In other words, the states most exposed to the subsidy cliff are also the states where national politics is always loud, close, and expensive.

Florida families and small business owners are doing the grim calculus

Kylie Barrios, a 30-year-old Florida resident, told CBS News she expects to be among those losing coverage. She said her family’s premium is effectively tripling, from about $900 in 2025 to $2,500 in 2026.

And while the policy argument in Washington often gets framed as partisan ideology, the personal argument sounds more like an invoice nobody can pay.

Barrios, who told CBS News she has generally voted Republican, described the mismatch between campaign promises and real-world bills: “The whole system feels as though it’s failed and isn’t advocating for me as a small business owner, as somebody who wants to become a mom and have a family.”

Congress tried two bills. Both lost

The political stalemate has paperwork behind it. In December, the Senate rejected two partisan health care bills, CBS News reported. Democrats pitched a three-year extension of the subsidies. Republicans offered an alternative centered on health savings accounts.

In the House, four centrist Republicans broke with GOP leadership to team up with Democrats and force a vote that could come as soon as January on a three-year extension of the tax credits. But the Senate’s rejection of a similar plan is the blinking warning light. Even if the House moves, it does not guarantee a landing.

Meanwhile, open enrollment remains in motion in many places. CBS News noted that the window to select and change plans is ongoing until Jan. 15 in most states, meaning final enrollment effects are still unfolding.

Why the timing matters: affordability is already the midterm battleground

The subsidy expiration hit at the start of a midterm election year, with affordability, including health care costs, high on voters’ lists of concerns, according to CBS News.

That makes this fight different from a typical Washington food fight. It has a built-in receipt every voter can pull up on a phone. Not a debate stage promise. A premium notice. A payment due date.

And it puts pressure on politicians who want to talk about the economy in broad strokes while millions of households are doing a narrow calculation: do we cover both parent and child, or just the child?

Provost told CBS News she hopes Congress revives the subsidies early in the year. If not, she said she would drop her own coverage and keep insurance only for her 4-year-old daughter because she cannot afford both at the current price.

What to watch next: a January vote, and a shrinking window for cover stories

The next milestone is the expected House vote in January on extending the credits. If lawmakers pass something that can actually clear the Senate, millions of families could get relief and Washington will declare it solved.

If not, the country moves into the next phase of the ACA affordability experiment: higher premiums, potential coverage losses, and a political blame game where every side has a quote and no side has a signed bill.

For now, the only certainty is the one delivered by the calendar. The subsidies expired. The prices rose. And the people most affected are the ones least able to treat health insurance like an optional line item.